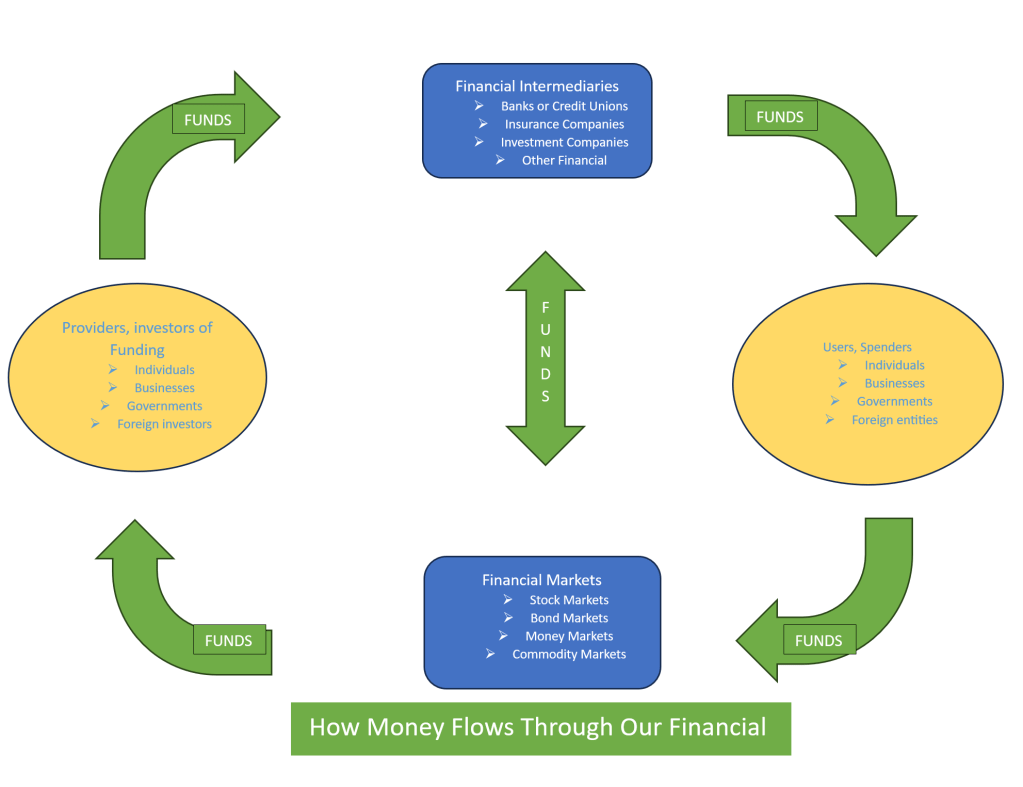

External influences affect the money flowing through our system and therefore we need to be vigilant and adjust our plans to reach financial stability. Not only do we need to watch what we are doing with our finances, we need to watch what everyone is doing with their finances as well. The ways other use their funds effects the amount we pay for our fund or receive for our lending.

Not only is our money supply effected by what happens in America, it is affected by global influences as well. At any given point and time there is only so much money made public. The forces of supply and demand come into play to affect the risk involved with lending that limited resource (money). The more people or entities demanding that dollar the higher it cost to borrow it. Then the lenders need to factor in the risk. Is it safer to lend to another government or a business.? Is it safer to lend to a business or to an organization? Is it safer to lend to an organization or a person? After these calculations have been determined the lending institution needs to factor in the percentage of profit they wish to make for bring the two (the savers and Borrowers) together.

The global influences on the dollar are caused by global economy influences. Not only are we in competition for the dollar so is the rest of the world. That being said we can understand the competition for the dollars as our companies compete for our business and the business in foreign countries. When our exports are lower in value than our imports than more dollars leave the country making those that remain more valuable. This affect reduces the funds available for our needs and desires. If foreign countries decide not to invest in America the domestic money supply is reduced further and causes interest rates to increase.

Most people are concerned with the buying power of their dollars. Inflation occurs when prices of items rise. In times of inflation the dollar loses value. An example would be you have $1,000, if you held on to that money for a year and the inflation was at 5% then you would need to spend $1,050 to purchase the same items which would have cost $1,000 a year prior.

Deflation can also occur. It is when the dollar becomes more valuable. Then you held onto that $1,000 but the was a 5% deflation. Then you would spend only $950 for the same items that would have cost $1,000 the year prior. Deflation is good but caution must be exercised. Sometimes people when they receive a salary increase go out and purchase a bigger house, a new sports car, and they put their selves deeper into debt. The trick is to maintain your lifestyle when deflation occurs to keep your living expenses low. Then you will be in position to take advantage of financial opportunities which come.

After WWII until the early 60s our annual inflation rate was in the 1 through 3 percent range.

Then in during the late 70s and early 80s it was in the 10 through 12 percent annual range. At the 12% range the dollar value had been cut in half. To see how fast your prices or savings take to double you may use the “Rule of 72”. Divide 72 by the annual inflation or interest rate.

An example would be:

72 divided by 3 is 24, thus it would take 24 years for your money to double.

72 divided by 12 is 6, thus it would take 6 years for your money to double.

It is because of these factors it is wise to develop and then achieve financial goals. Lack of doing so explains why some people have money problems. They are the victims of the lack of planning and weak money management habits in the areas of spending and the use of credit. Another factor is the marking success of companies and the campaigns which encourage people to overspend. The Path to financial well being begins with clear financial goals.

What are the financial goals which you have sat for yourself?

Goal setting is foundation of financial Planning. Without goals there is nothing to plan. There is an old saying which says, “If you don’t know where you’re going, you might end up somewhere else and not even know it.” Your goal is how you can determine your progress of your spending, savings, and investing set goals that can answer the question of “why”. If you don’t know the why behind your goal, you may have set an inappropriate goal. When setting our Goals, we need to take the SMART approach.

An example of the SMART system

| Specific | Create an emergency fund |

| Measurable | I will save $2,500 for a new computer |

| Action- Oriented | I will transfer my fund from the bank and place them in the credit union |

| Realistic | I will save this by reducing the times I eat out |

| Time Based | I will purchase the new computer system within a year |

Evaluate your current financial activities to achieve your goals. If you answer yes to eight of these you have a strong personal finance system in place.

Image by Drazen Zigic</a> on Freepik

| YES | NO | ||

| 1 | Have you created your budget or spending plan to guide you financial activities? | ||

| 2 | Each month do you pay your bills, and credit card on time? | ||

| 3 | Do you keep a record of the amount spent on various items throughout the month? | ||

| 4 | Is your monthly spending less than your income? | ||

| 5 | If an unexpected major came up do you have the funds to cover the cost? | ||

| 6 | Do you have a daily spending limit/weekly limit? | ||

| 7 | Do you have money set aside each month in a savings or investment account? | ||

| 8 | Does your record keeping system allow you to locate important documents? | ||

| 9 | Do you know the balance of your credit card accounts and other loans? | ||

| 10 | Over the past 360 day have you successfully avoided late fee on credit cards, loans and bills? |

No matter what you do with your finances there are two things you will pay neither of which are death or taxes. They are:

- Time Value of Money: (TVM) is the concept that money you hold today is worth more than money you receive tomorrow.

- Opportunity Cost: Opportunity cost is what you give up by making your choice

In practice these are more complex than what they first appear. The Time Value of Money concept isn’t based on inflation. It is based on the fact that the money you hold today can be put to work earning you more money.

Opportunity cost however is based on the fact that you can’t do two things with the same dollar.

If you have ten dollars you could use it to buy gas for your car or you could walk, you could also use it to buy food for the day, but you can pay for ten dollars of gas and then purchase the days food with the same ten dollars. The other thing you could do with the ten dollars is keep it. You could walk were you need to go and chose to not eat or walk to a friends or family member’s home and eat with them.

If you have ten dollars today and the interest the bank pays is .03 percent per year then next year if you still have the ten dollars, you’ll have $10.00 X .03 + $10.30

Personally, I use the BAII plus Texas Instrument calculator for these problems

In the third row there are five buttons. They read n, I/Y, PV, PMT and FV from left to right.

N = the number of payments being calculated

I/Y = is the interest being paid

PV = is the present value

PMT =is the payment

FV= is the future value

Therefore, I would first clear the calculator.

Press the number 1 then N

Press the number 3 then I/Y (The calculator knows it’s a percentage.)

Enter 10 by pressing two numbers and then the PV button

Once this is accomplished you go to the top row on the far left is a button that reads CPT which stands for compute. Press it and then press the FV button, it should give you the 10.0000 you need two round the number off to the decimal you prefer. The calculator is easy to use and there are plenty of YouTube videos to show you how to do the more complex problems.

Note: I am not an T I employee and have received no funding for recommending their produce. You are free to use any financial calculator you wish or do the math using the formulas. Weather or not you purchase the T I calculator is your decision and your responsibility.

Leave a comment